Who can claim a VAT refund

Vat Refund Payment Methods

For refund amount not exceeding 30,000 baht, the refund payment can be made in the form a

1.1 Cash (Thai baht only) or

1.2 Bank draft in four currencies: US$, EURO, STERLING, YEN or

1.3 Transfer into Credit card account (VISA, MASTERCARD, and JCB)

2. For refund amount exceeding 30,000 baht, the refund payment can be made in the form of bank draft or transfer into a credit card account (as detailed in 1.2 and 1.3)

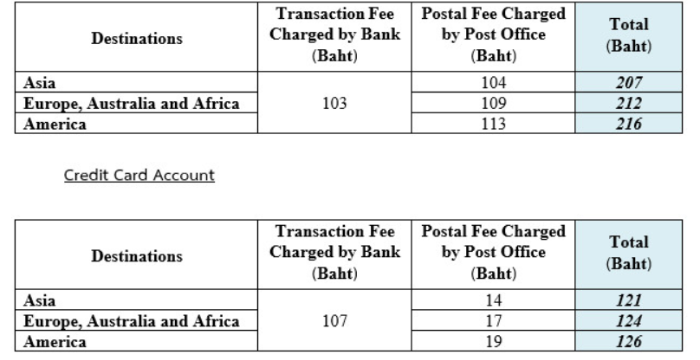

The expense consist of draft or transfer fee, and postal fee which are charged by banks and post office and they will be deducted from the refund amount. Below tables are shown the approximately rate of the expenses.

*The postal fee depends upon distances and weights of the letter

Why the VAT refund are disapproved